📊 Full opportunity report: The Sovereignty Dilemma In Mistral’s European AI Strategy on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

Mistral has achieved rapid revenue growth and European valuation, but faces critical challenges in model performance, infrastructure dependence, and maintaining sovereignty amid US and Chinese competition. Key developments include model gaps and financial opacity.

Mistral, a European AI startup valued at over €11.7 billion, is experiencing a strategic dilemma as its rapid growth and European identity are increasingly tested by model performance gaps and reliance on non-European infrastructure, raising questions about its sovereignty claims and long-term competitiveness.

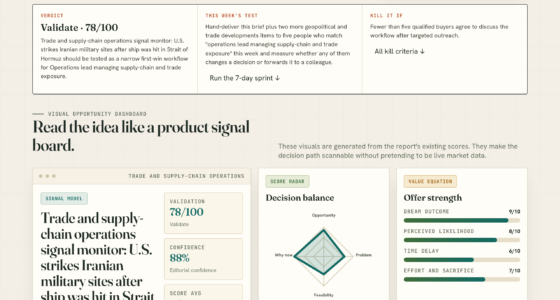

Founded with a focus on maintaining European data sovereignty, Mistral has grown its annual recurring revenue from roughly $16–20 million at the start of 2025 to over $400 million by January 2026, driven by major enterprise clients such as HSBC, Airbus, and the French armed forces. You can learn more about Understanding Mistral’s AI Rise: A Sovereignty Challenge For Europe. The company raised approximately $3B to $5.5B in funding, with a valuation reaching roughly $23 billion. Despite this, Mistral’s business model relies heavily on non-European infrastructure, including cloud services from Azure, AWS, and Google Cloud, and silicon from Nvidia.

While the company claims to prioritize European data sovereignty, nearly 40% of its revenue is generated outside Europe. For more context on this issue, see Different Game, or Already Lost? Reading Mistral’s Sovereignty Bet. Its model performance remains below US and Chinese competitors, with third-party assessments indicating its models lag in speed and accuracy. To explore this further, see Understanding Mistral’s AI Rise: A Sovereignty Challenge For Europe. Mistral’s flagship model, once touted as open and European, now faces stiff competition from open models like GLM-5.2 and Kimi K2.6, which outperform it on key benchmarks. The company’s financial opacity—including undisclosed losses and high capital-to-revenue ratios—adds to governance concerns, especially as it explores AI chip development amidst a fierce hardware race.

Mistral’s sovereignty paradox: a critical look at Europe’s AI champion

The growth is real and rare — $16M → $400M+ ARR in a year. But the moat is narrower than the story, the open-weight advantage is gone, and the company selling purity has a purity problem. When your product is sovereignty, every impurity costs more than it would for anyone else.

- The open moat is gone — GLM-5.2, DeepSeek V4, Qwen, Kimi are open and better; now Inkling too

- Large 3 below median on AA index for peer open models; ~38 tok/s

- Vibe/Le Chat badly behind ChatGPT & Claude — even at Station F, Paris

- No loss figures ever disclosed; ~$3–5.5B raised vs $400M ARR

- Own-chip ambition = distraction at this scale

- Great API pricing — but price is the most copyable moat

- The “default second model” in multi-provider stacks = commodity position

- Voxtral trails ElevenLabs; Devstral behind coding agents

- Studio / Workflows / Agents undifferentiated vs Foundry, Bedrock, LangChain

- Ministral fine at the edge

- SecNumCloud — US hyperscalers structurally cannot hold it

- Defence: French armed forces framework deal; Helsing

- Industrial/physical AI — Emmi, Airbus, BMW: Europe’s real home turf

- Non-compute-bound wins: OCR 4 (170 langs, self-host), Leanstral (SOTA, ~1/75th cost)

- “The rest of the world” — states wanting neither DC nor Beijing

It looks like chaos — 18+ products for 350 people. Two things are true: it’s consolidating (Small 4 merged Magistral+Pixtral+Devstral; Le Chat → Vibe), and the real plan is vertical integration of the whole sovereign stack. Mensch at VivaTech: moving “from an AI company doing software to a cloud company.”

Mistral is the most important test running on whether European AI sovereignty is a business or a subsidy. The demand is real, the legal wedge is durable in 3–4 verticals, the growth is extraordinary. But the open-weight moat is gone, the vertical integration is being attempted from behind on six fronts, and April’s Cohere–Aleph Alpha merger killed the “only credible European option” claim. Stop trying to be Europe’s OpenAI. Finish being Europe’s Palantir. Own the narrowness — it’s a better business than the one being marketed. And watch the $1B ARR number in December: that’s the honest scoreboard.

Implications of Model Performance and Sovereignty Claims

This situation underscores the tension between European sovereignty and the realities of global AI infrastructure. Despite its branding, Mistral’s reliance on US and Asian cloud and silicon supply chains exposes its strategic vulnerabilities. The company’s technical lag behind US and Chinese models questions its ability to sustain a European-led AI ecosystem. Financial opacity and high capital requirements also pose risks to its long-term viability, potentially impacting Europe’s position in the AI race and the broader debate over data sovereignty.

European data sovereignty cloud services

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

European AI Ambitions Amid Global Competition

Since its founding, Mistral has positioned itself as a European challenger to US and Chinese AI giants, emphasizing data sovereignty and open weights. Its rapid valuation growth and enterprise client base reflect strong market interest. However, the broader AI landscape is dominated by US firms like OpenAI and Anthropic, which hold dominant market valuations and technical leadership. European AI efforts face challenges in model quality, infrastructure dependence, and developer engagement, with Mistral’s performance lagging behind open models and its consumer product struggling for adoption. The company’s strategy to develop AI chips further complicates its focus and resource allocation, amid a global hardware arms race.

“Roughly 40% of Mistral’s revenue comes from non-European clients, despite its European branding.”

— Arthur Mensch, Forbes

AI model performance benchmarking tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Aspects of Mistral’s Long-Term Strategy

It remains uncertain whether Mistral can close its model performance gap quickly enough to maintain its competitive edge and uphold its sovereignty narrative. The company’s plans for developing AI chips and expanding its product line are still in early stages, with no clear timeline or proven viability. Additionally, the impact of financial opacity and potential losses on future funding and market perception is not yet fully understood. The extent to which Mistral can reduce its reliance on non-European infrastructure remains an open question.

enterprise AI security hardware

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Upcoming Milestones and Strategic Developments

Next steps include Mistral’s efforts to improve model performance through technical upgrades and potentially expanding its open-model ecosystem. The company is expected to clarify its financial position as it approaches its self-imposed $1 billion revenue target by the end of 2026. Watch for updates on its AI chip development plans and how these efforts impact its technical leadership and sovereignty claims. Additionally, the company’s ability to attract European developer engagement and compete with established US and Chinese models will be critical to its future trajectory.

European AI infrastructure solutions

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Can Mistral truly claim European sovereignty given its reliance on US infrastructure?

While Mistral emphasizes its European origins and data policies, nearly 40% of its revenue comes from outside Europe, and it relies heavily on US cloud providers and hardware, complicating its sovereignty claims.

Will Mistral be able to close its model performance gap?

It remains uncertain. Technical assessments indicate its models lag behind US and Chinese competitors, and efforts to improve are ongoing but unproven at scale.

What risks does Mistral face from its financial opacity?

The lack of disclosed profit or loss figures and high capital-to-revenue ratios pose governance and funding risks, especially if losses continue or grow.

How might Mistral’s chip ambitions influence its competitive position?

Developing proprietary AI chips could offer strategic independence but currently represents a costly distraction without immediate technical or market advantage.

What is the significance of Mistral’s consumer product, Vibe?

Vibe has limited market recognition and user engagement compared to competitors like ChatGPT, indicating challenges in establishing a strong developer or user base within Europe.

Source: ThorstenMeyerAI.com